BURST

BURSTLots of monopoly news, as usual. Five Senators introduced legislation to break up the big meatpackers, Ticketmaster faced heat as its business practices were put on the stand in front of a jury, there was a terrible jobs report, and Hollywood is having trouble opposing the Paramount-Warner deal, though it may fall apart because of financing woes.

Before getting to the full round-up, I want to do some analysis of the economic effects of the current conflict in the Middle East. Because that’s obviously the biggest news story going on.

One odd part of this situation is how little the financial markets have reacted. While the stock market was down last week, it was only a modest decline. Clearly participants in the capital markets just didn’t think the war was breaking anything important. Maybe they were right, or maybe it’s similar to the pre-Covid period, before markets went haywire. That said, the signs right now suggest that dynamic might be shifting.

I found last week’s broader calm in the financial markets unsettling. If this conflict doesn’t end soon, the risks of a serious economic crisis are increasing. An oil price shock in this globalized system is unpredictable. Such a shock will likely turn into a supply chain disruption as fossil fuel dependent industries - aka everyone - suffer. There are also secondary financial risks, because oil states who can no longer ship oil need money, which means they may have to stop financing activities and sell their U.S. investments. And these pressures are operating on a corporate system that is inflexible and poorly regulated, which will compound the problems. Finally, there hasn’t been a meaningful financial downturn in years, so there’s likely lots of froth and fraud in our markets. And that’s likely to be exposed as well.

Let’s start with the oil shock and resulting supply chain crises.

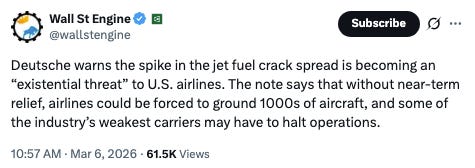

When the price of oil goes up quickly, a host of industries suffer. Take an obvious problem - flying. The cost of fuel is between 20-30% of the operating cost of an airline. The price of jet fuel in Singapore, a major hub, has doubled since the U.S. attacked Iran. This increase is going to spike airline prices dramatically, while at the same time weakening the industry financially.

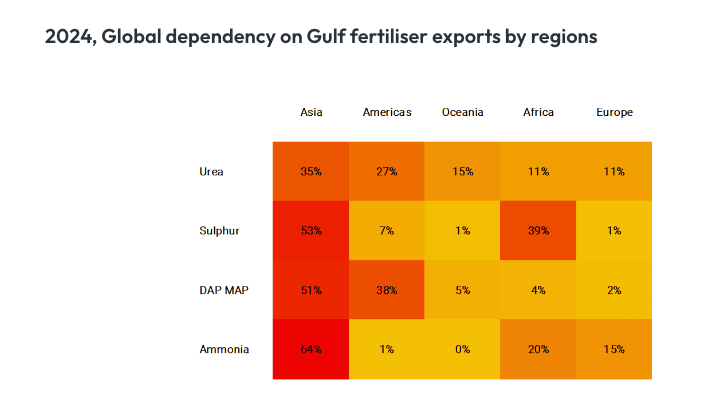

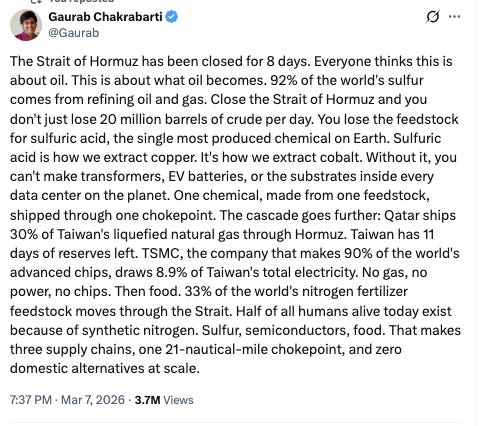

Then there’s farming. The Straight of Hormuz handles a third of the trade for fertilizer. And it’s spring planting season in the northern hemisphere. American farmers are already having trouble because of high input costs, with farm bankruptcies rising. So this situation is not great.

You can go down the list of industries. Shipping and trucking are fuel-dependent, same with petrochemicals and plastics, both of which go into semiconductors. Fairly soon, East Asian nations on whom we depend for everything from medical supplies to bibles can no longer import necessary fuel from oil-rich Arab states.

Then there are the financial consequences. The big gulf states - Saudi Arabia, Qatar, UAE, and Kuwait - can’t generate income, but must pay for their state budgets. So they are exploring how to sell the financial assets they own in the West.

“A number of Gulf countries have begun an internal review to determine whether force majeure clauses can be invoked in current contracts, while also reviewing current and future investment commitments in order to alleviate some of the anticipated economic strain from the current war,” said one Gulf official. “Especially if the war and related expenses continue at the same pace.”

How significant are these investments?

It’s hard to tell, but the oil-rich countries are a central part of the Trump administration economy strategy. Last May, Trump returned from the Middle East having “secured” $600 Billion in investment commitments from the Saudis, $1.2 Trillion from Qatar, and $1.4 Trillion from the UAE. These numbers are a lot of hype, Arab investors have financed a good chunk of the AI investments, the Paramount bid for Warner, Elon Musk’s takeover of Twitter, the leveraged buyout of Electronic Arts, an attempted acquisition of the PGA Tour, and endless promises to build data centers.

In terms of prestige, Trump secured puffery-style statements on Middle Eastern investment from leaders of Google, Amazon, Oracle, GE Vernova, Palantir, Lockheed Martin, L3 Harris, Bechtel, Franklin Templeton, Qualcomm, Boeing, Northrop Grumman, Occidental Petroleum, Baker Hughes, and dozens of others. So a lot of powerful U.S. corporate executives think oil state investment matters.

More broadly, while a lot of foreign policy thinkers talk about allies, the truth is that American alliances are anchored by foreign ownership of the U.S. stock market. We supply the dollar denominated assets and a place they can buy and sell them, at will. There are $35 trillion of equity investments in the U.S. held by foreigners. If the Iran war causes foreigners to need to sell their assets, the stock market will decline. And for better or worse, mostly worse, most American institutions, from universities to governments to corporations to the AI investment frenzy, are directly or indirectly dependent on a high stock market.

And that brings us to the effects of these shocks on our markets.

A Concentrated Set of Supply Chains

During the Covid crisis, I noted repeatedly that decades of monopolization and bad regulation have thinned out our supply chains and created a lot of fragility in corporate America. After Covid, we did a few things, like moving some chip production to the U.S., but mostly did little. The reason is that the lodestar for our economy is still promoting the efficiency of capital, and that means continuing to thin out how we make and move things.

Let’s go back to the airline industry. Prior to 1978, the U.S. carefully regulated prices and costs, kept a reasonable slack, and ensured that airlines had to let passengers from different airlines fly on their planes, if necessary. The benefits of scale were available to all. The air grid could manage demand and supply shocks.

That’s no longer the case. After 9/11, airlines experienced a wave of bankruptcies, followed by consolidation. And now larger firms have all sorts of advantages. Financing costs are lower for the big guys, they have better access to airport gates and slots, they use frequent flyer programs to lock in customers, and they use their scale to thwart smaller competitors. So with airlines, since Covid, the industry in the U.S. has split between the profitable top four trunk airlines, led by United and Delta, and the unprofitable everyone else.

So what happens with this Iran price shock? I can imagine a number of scenarios. The best case is simply that prices go up and consumers keep paying, leaving the industry unchanged. The worst case is prices go up, demand goes down, and most of the industry goes bankrupt, followed by consolidation and then ultimately a much smaller and pricier airline grid. If that happens, it’ll just be hard to fly places in America.

As with airlines, so too with a host of industries.

I mentioned farming. The biggest input cost after labor is energy, so the Iran situation isn’t good for food production. The U.S. agricultural system used to be regulated to manage supply shocks, we would stockpile when times were plenty, and could lower stockpiles when they weren’t.

Indeed, the name for the New Deal system was called “supply management,” because it had the government work cooperatively with farmers to balance production, pricing, and conserving the land. We kept tight control of inputs. Tennessee Valley Authority, a government run giant utility, produced a lot of fertilizer.

But prudent public management of resources and markets no longer exists. Instead, farming is now on a boom and bust cycle, like airlines. In bad times, land just flows into the hands of oligarchs, which is why Bill Gates is now the largest private landowner in America.

And that’s just talking energy. Taiwan doesn’t have much in reserves of natural gas, it is wholly dependent on Middle East imports. And every industry, from toys to cars, must get chips from Taiwan. So… that’s a problem.

More broadly, every corporate officer in every large corporation is right now looking through their supply chains, examining vulnerabilities, and exploring opportunities. What are those opportunities? Well, we saw during Covid, it was increasing prices faster than costs to take advantage of the narrative of shortages.

Oh, and there’s one more dynamic. Since the financial crisis of 2008, financial markets have moved mostly upward. After Covid in 2020, there was a great bailout of all financiers, once again. Indeed, any time there have been problems - as with Silicon Valley Bank - they got bailed out. The net result is that bankers have likely lost discipline in underwriting, and there’s likely a lot of fraud in the financial system. The chatter on Wall Street is that it’s in the multi-trillion dollar “private credit” market, an opaque area with lots of self-dealing. That seems likely. But it could also be in many other unexpected places.

So this Iran conflict worries me. It’s a lot of risk. I hope it is short, because the longer it goes on, the longer it seems likely that something important will break.

On the other hand, a downturn opens the door for a different form of economic governance. After 9/11, the Iraq War, the crisis of 2008, and Covid, policymakers mostly sought to double down on existing systems of power. More surveillance, more consolidation, less democracy, more finance.

In part that’s because there was no competitive set of ideas, what Margaret Thatcher once called TINA - There Is No Alternative. In 2008, there just weren’t any populists who could, say, reorganize the banking system, and the public hadn’t considered whether it was necessary to do so.

Today that’s no longer true. A large chunk of our political order has been exposed to anti-monopoly concepts, and the public has turned against the Epstein class writ large. So industries in crisis may request a bailout, and this time, at least some people will know what to demand. There are much darker possibilities as well, but that is at least a foundation for optimism. Yes it’s thin, very thin. But it’s not nothing. Every time we refuse to learn our lesson, we’ll get kicked harder. Hopefully we’ll learn it this time.

And now, the rest of the round-up. There are some important updates of the Paramount-Warner deal. Opposition to the deal is fractured, but Larry Ellison’s net worth has collapsed since he started bidding. Plus, top Democrats embrace a legislative break-up of big meatpackers, Corpus Christi may run out of water, Dr. Oz actually cracked down on corrupt health insurers, and for a time, Polymarket let people bet on whether there will be a nuclear war. Awkward!

All that and more after the paywall. This stuff is getting more important and scarier.