BURST

BURSTIn 1981, a consultant named Elmer Smalling, an expert in pay-TV systems, was negotiating on behalf of Jefferson City, Missouri, to see about better prices for residents. Across the table was an executive for a giant corporation named TCI, which had 25% of the U.S. cable market and was known for the hard-charging tactics of its CEO, John Malone. The negotiations were not going well, because the city was thinking of taking away the franchise and going with someone else. Paul Alden, one of Malone’s subordinates, lived up to that reputation.

“We know where you live, where your office is and who you owe money to,” he told Smalling. ”We are having your house watched and we are going to use this information to destroy you. You made a big mistake messing with T.C.I. We are the largest cable company around [.] We are going to see that you are ruined professionally.”

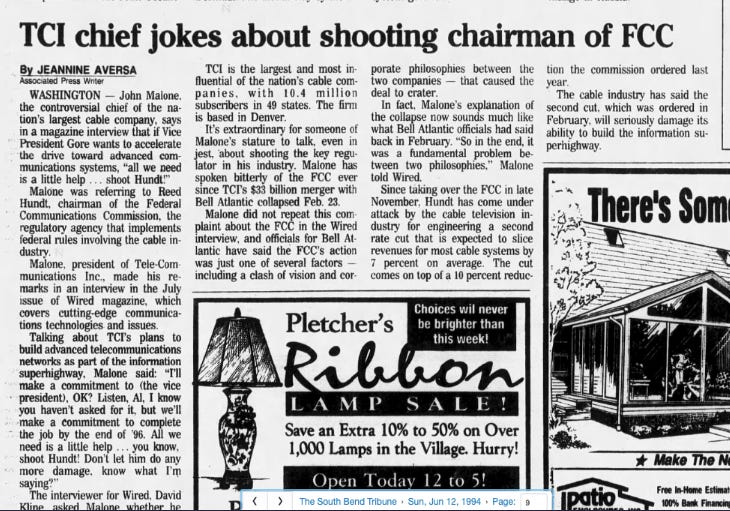

A few years later, Malone did it again. Frustrated at regulation, he mused publicly about shooting Bill Clinton’s Federal Communications Chair, Reed Hundt, in order to deregulate the industry, and speed up the deployment of advanced telecommunications networks. At the time, this joke about murdering his overseeing was quite controversial; Malone had to apologize.

After this litany of threats, I’d like to say that Malone was pushed out of American business in disgrace, a would-be mobster. But Smalling lost clients, TCI got its Jefferson City franchise renewed, and the media and broadband were deregulated. Today, Malone is one of the wealthiest and most powerful men in the world, a culture-definer for American business, and a “legend” in deal-making, according to Dealbook’s Andrew Ross Sorkin. You may not have heard of him - an intentional choice on his part - but he matters.

One of the things you start to hear a lot when you write about monopoly is some variant of the comment, “Wow, that seems like the mob.” The arbitrary coercion that is now a part of commerce was not always normal; it certainly wasn’t routine in the 1950s, when the mob, with its control of gambling, was very distinct from legitimate business.

But when did this transition happen? And who organized it? Part of the story is the Chicago School academics who took over policy, the Robert Bork shift in antitrust frameworks towards the efficiency of capital. But there were also men in business who orchestrated it in how they wrote contracts, how they hired people to string wires, and how they reorganized the American media. They used the new legal frameworks to amass vast wealth and power, and reinforce what Bork was doing.

John Malone is a leader of these men, whose likes include Rupert Murdoch, Barry Diller, Craig McCaw, Sumner Redstone, and Ted Turner. This group bridged the era of middle class control of politics to today’s oligarchy. And they built their fortunes in the media and cable systems, which were transforming in the 1970s from a New Deal model to the deregulated framework of today. They are the predecessors of today’s tech oligarchs, the Jeff Bezos, Mark Zuckerberg and Elon Musk’s, who were born after the Bork revolution had won. Malone walked, so Zuckerberg could run.

I watched Malone interviewed six months ago on CNBC, and deferential does not begin to describe the approach of the anchors. They addressed him as a lordly figure, sitting on his every word, like a lesser known Warren Buffett. As Deadline wrote, “The semi-reclusive mogul is probably the closest thing the media business has to an oracle.”

While Malone normally eschews publicity, that day he was on CNBC because he was doing us a favor. He was releasing his autobiography, Born to Be Wired: Lessons from a Lifetime Transforming Television, Wiring America for the Internet, and Growing Formula One, Discovery, Sirius XM, and the Atlanta Braves.

And this book, while not honest, is as close as I’ve ever seen to getting to the core of how the billionaires who took over American society really think. Malone’s book helped me understand the generation of media billionaires, before the tech oligarchs, who had to contend with the dying embers of New Deal regulations. And they knew a world where it wasn’t ok to do what they were trying to do, and yet they did it anyway, with energy, creativity, and a malevolent zeal to make the world safe for capital.

I don’t normally do book reviews for BIG. But this time, I’m making an exception. Because Malone has given us an explanation of what we are really up against.

The first thing to understand about Malone is that he is not a liar exactly, but he is also not a credible narrator. The Jefferson City negotiation was an important moment, showing how ruthless he is. “Was I a tough negotiator?,” he wrote about this period in his life. “Damn right I was.” But that particular story is not in his autobiography.

Indeed, Malone presents the episode entirely different, portraying himself as a painfully shy man set upon by publicity hungry politicians. He talks about testifying at a Senate hearing in 1989, where Senators unfairly bashed him for just trying to deliver a technologically advanced entertainment product to Americans.

“Cramped and sweating at a table before Senators questioning the industry’s pricing power,” he wrote, “in a gallery filled with people, including the press. Quite literally, my worst nightmare.” The entire ordeal was a “public humiliation.” Senator Al Gore likened him to “King of the Cable Cosa Nostra,” like the Mafia, or alternatively, to Darth Vader. It was poor painfully shy Malone, against a phalanx of mean politicians.

“TCI,” said Gore, “is obviously hell bent towards total domination of the market as it buys up not only more and more cable systems, but more and more programming services, and even movie studios.” It was unfair treatment, Malone notes, but said he didn’t respond to Gore’s provocations. “You cannot win a pissing contest with a skunk,” he wrote.

Readers of Malone’s book, mostly the CNBC set, will no doubt chortle, but I know Gore as a savvy politician. And that’s why I decided to check out the hearing from 1989, to see if the book was accurate. And it turns out, it was not. Not that Malone said anything that wasn’t true, but he neglected to include why Gore called him a mafioso. So when I watched the hearing, with TCI threatening Smalling, it made sense. And Malone responded to Gore about that story, obviously pained he had been caught. You can watch it right here. It’s stunning.

One of my contacts in the telecom world, after I showed her the video clip of Gore confronting Malone, texted me back, “Unfortunately typical for cable cos.”

What brings about such a mindset, a brilliant and sparkling authoritarianism? There’s enough in his autobiography to understand his thinking.

Malone was born in Connecticut in 1941 to a Calvinist family, the son of a General Electric engineer, an early tinkerer with the technology of television and a man so unflappable that his nickname in the neighborhood was the “gentle giant.” His shared love with his father was mechanical engineering, from cars to TVs, and Malone still finds excitement in cars today. A shy, introverted, and highly focused kid, Malone wrote that “I could explain far more easily how to rebuild a carburetor than tell you how I was feeling at any given moment.”

Today, Malone recognizes in his father, and then himself, a form of Asperger’s syndrome, an inability to intuitively connect with other human beings. Yet he saw this emotional detachment as a superpower; “My autism has gifted me with the ability to hyper-focus on intricate challenges and pursue a goal with dogged determination. I saw patters, connections, and solutions others overlooked… With a virtual photographic memory at the time, I could recall verbatim entire sections of books.”

This book is supposed to be about business, but a severe religious belief in efficiency colors its intensely political framing. In his childhood, Malone was athletic and studious, attending a boarding school and then Yale in the early 1960s, where he discovered a loathing of Keynesian economics. “I believed in free markets,” he wrote about his libertarian views. “To me, people act in their own self-interest, it’s just human nature, and that’s what drives the economy.” To Malone, it’s a dog-eat-dog world.

After Yale, Malone went through the most prestigious corporate institutions in America, working at AT&T’s iconic Bell Labs. While at a scientific lab at the height of its power, a place where researchers discovered such foundational aspects of our universe like the big bang, and invented devices like the laser and the semiconductor, Malone’s passion drew him not to the scientific future but to the financial future - financial engineering. He focused on the theory of business operations.

At age 27, he presented to the AT&T board of directors something that was then novel in corporate governance. He argued for them to buy back their own stock, which would reduce the total number of shares and thus increase earnings per share. The Chair of AT&T at the time, Fred Kappel, rejected the suggestion, while congratulating Malone on a fabulous presentation. Kappel told him, “If in your whole career, you can do a single thing that changes the Ma Bell system in even the smallest way, you would be very successful.”

It was a jarring moment for Malone. Though a rising star at AT&T, he realized he’d have to leave Bell Labs because it wouldn’t satisfy his need for control. But it’s also, unwittingly, the moment we see a young aggressive corporate leader’s reaction to that of an executive who was genuinely engaged in caretaking of a vast enterprise. Bell Labs had violated what would become a cardinal rule for Malone, which is that its leaders valued the corporation itself over the efficient use of capital in maximizing returns. Malone told his colleagues that Bell Labs, the legendary scientific lab, was a bureaucratic mess, a dinosaur, headed for extinction.

When he left Bell Labs for McKinsey, Malone writes as if it is an act of rebellion. “I wondered whether I had just jumped from the biggest, safest vessel I would ever board,” he wrote, “I felt ill.” This kind of odd faux rebellious streak courses through the book. Meetings where a banker decides to lend or not to lend to multi-millionaires become tales of risk and heroism. Here’s one of many intolerably cliched sentences - “Craig McGraw ate risk like Corn Flakes for breakfast every morning” or “We pinched pennies so hard you could hear Lincoln cry.” Random business people he likes are described as cowboys and former fighter pilots, while politicians are mostly blustery morons. He talks of financial metrics with the tone of a lover, while his children are mostly people he missed growing up as he travels from city to city as a conquering financier.

By the early 1970s, he wound up as an executive for one of his clients, Jerrold Electronics, which made equipment for the cable industry. His insight to increase profitability was to move the company’s plant from Philadelphia to Mexico, because he says, America couldn’t make low cost products efficiently. The mass layoffs led to an increase in profit margins. In some ways, Malone seems to be a disease vector for many of the ills that corporate America foisted on Americans from the 1960s onward.

Malone then joined TCI, a Colorado-based cable firm. A pioneer in offshoring at Jerrold, Malone then pioneered the roll-up strategy at TCI, acquiring 482 companies from 1973-1989, “a rate of new deal every two weeks.” The “key to victory at TCI was in our ability to gain scale and grow ever larger through acquisitions.” He also innovated around financial engineering, noting that cable systems had a tax advantage over phone companies and so could artificially depress earnings and thus taxable income. He popularized the now ubiquitous term on Wall Street EBITA (Earnings before interest, taxes, and amortization), preaching that it was a better metric than net income, because it helped companies avoid taxes. He issued another innovation, the “tracking stock,” allowing investors to buy into one specific line of business.

It was in this period that the threats to Jefferson City occurred. How many other stories did he leave out? How many lives were wrecked through these tactics? Malone writes as if he was proud of coercion; he goes into ways he compelled city councils by turning off cable systems and pointing viewers to their local politicians as a way of blaming them for losing access to TV.

By the early 1980s, his pursuit of scale and power had paid off; TCI owned a little less than a quarter of the cable market, and as he noted, “cable had become a natural monopoly.” But the big three TV networks loomed as dominant regulated players. So Malone backed an entrepreneur named Ted Turner, who sought to use satellite technology to break the control of the big three traditional networks and deliver new channels to cable networks, like SuperStation TBS and eventually CNN. It kicked off a boom in cable channels.

TCI, whose network could make or break one of these new endeavors, was in a prime position. Malone had his company take ownership stakes in a whole series of cable channels from the Christian Broadcasting Network to Black Entertainment Television. It didn’t own them outright, for fear of antitrust enforcers. Eventually, Malone spun out the media content of TCI into his own personal investment vehicle, Liberty Media, which became a holding company for an endless set of investments: first channels like CNN, American Movie Classics (AMC), the Family Channel, QVC, and Starz, but eventually stakes in larger entities like Live Nation, Expedia, DirectTV, SiriusXM, Formula One, and Discovery Bros Warner.

Malone was an obsessive about dominating the competition. “I had no time,” he wrote, “for TV shows, the bar, or even my family for that matter.” His desire to win, to acquire, superseded all else. Indeed, the man shaping the American media experience is a finance obsessed guy with Asperger’s who was doing so many mergers and acquisitions he didn’t have time to watch tv or movies. That’s a far cry from the days of Hollywood tycoons, who for all their bad behavior, genuinely thought about the underlying product. His love was a sort of financial authoritarianism, making the number go up at all costs.

In 1984, the Reagan administration deregulated the cable industry with the Cable Communications Policy Act of 1984, removing pricing control and regulation from local municipalities. Prices exploded, jumping 61% in just a few years, and service quality declined. Malone wrote that he was “so focused on growing the company that I ignored how poor our customer service had become.” Complaints piled up on Capitol Hill, with TCI as a main villain. And that’s what led to the infamous hearing and back-and-forth with Gore that he leaves out of his book.

Another story Gore relayed is how NBC wanted to compete with CNN, but Malone told them not to. TCI was an investor in CNN, so it preferred not to have competition. Instead, Malone had NBC pay TCI millions of dollars for an unused channel, and create a financial news network that wouldn’t compete with CNN. That is the origin story of CNBC.

At one point in the hearing, Malone argued that TCI was not particularly profitable in terms of net income, when he knew that was not a meaningful metric. A southern courtly Senator, Fritz Hollings, responded by asking him about the appreciation of TCI’s stock price, which made the ruse obvious. Everyone laughed. So perhaps it was a public humiliation. It was not, as Malone writes, because he is shy or politicians were grandstanding, but because he was evasive and dishonest. As he left, Hollings said to him, grinning, “John, you know even Thomas Edison had to accept the fact that he was gonna be in a regulated industry.” To the politicians at the time, public control of corporations was part of the natural order, and always had been.

The result of the hearings and controversy was the Cable Act of 1992, which had the government set prices and imposed a variety of public utility rules on the industry. Prices dropped by 17% in the first two years. According to a then-regulator I asked about this episode, the pressure these rollbacks induced forced cable magnates to find another use for their networks, ultimately leading them to introduce digital TV and eventually cable modems. But Malone doesn’t give credit for that innovation to regulation, instead suggesting it was his own industry’s brilliance.

Malone is a libertarian who helped reorganize American culture through cable, but he eventually came upon a force bigger than his own industry - Silicon Valley. In the mid-1990s, it became clear that cable could be an on-ramp for the nascent internet.

At the time, Bill Gates offered Microsoft software to run the entire industry, from servers in the cable headend to set top boxes. He had billions in cash lying around, and put $1 billion into Comcast. Wall Street got excited the richest man in America was interested in this capital-heavy business. In return for Microsoft’s participation, Gates demanded a fraction of all revenue earned in interactive services, a “vig,” as the mob would put it. The cable magnates turned him down. “Bill has got to accept the fact that he can’t set the standard that the rest of us are going to use,” said Malone.

In the late 1990s, Malone, no longer a young man, began staking other important would-be media barons. Barry Diller became the CEO of a company Malone set up for him, which turned into USA Networks, then Universal, then InteractiveCorp, and finally IAC. He organized a takeover of Ticketmaster, and in 1999 the roll-up of data services through the Match Group. He was a player as his friend Ted Turner enabled the AOL-Time Warner merger, he introduced Fox News by carrying Rupert Murdoch’s new channel, and he sought the services of Michael Milken’s junk bond empire.

The last part of the book shows a Malone retreating into old age. “There was so much stress… that I literally flinched when I peeked into my mailbox, afraid it was a letter from the IRS or the FCC or the DOJ.” In the 1990s, Malone pulled back a bit from his role as a CEO, listing out a series of life goals. Three are worth mentioning. “To ensure a safe and liquid personal investment portfolio.” “To reduce government, media, and legal exposure by removing myself from the public eye.” And “generate predictable income.” He also talked often with his partner, Bob Magness, over “estate taxes and how to avoid them.” Malone soon became the second largest private landowner in America, wealthy beyond imagination, and out of the limelight even as he negotiated deals that reorganized American life.

It wasn’t a pleasant book to read, and it was hard to keep track of all of Malone’s business empire-building moves. He helped organize the Live Nation-Ticketmaster merger, which he called an “unavoidable natural evolution of business.” He did tracking stock after tracking stock, he staked Barry Diller, cooperated and fought with Rupert Murdoch, and hired and oversaw Discovery and then Warner CEO David Zaslav. His libertarianism, that sense of inevitability that guided his actions, was the attitude of a zealot.

The most discordant part of the book is Malone’s chapter on big tech, when he suddenly embraces government action. He describes his one meeting with Mark Zuckerberg, when Malone asked why he sought to acquire rivals instead of buying smaller percentages of them. “Well I don’t know why I would do that when I can sort of own everything,” Zuckerberg responded. “At least for now, I’m not facing any government pushback as I try to buy things like WhatsApp or Instagram.”

Malone was shocked, realizing government had been lax in addressing those dominant firms, who never were subject to the kind of regulation he had to face. Now it’s too late for competition to work. “We need a new regime,” he argues, “for government regulations designed to rein in and monitor the gigantic companies of Big Tech - the biggest, most powerful corporations ever to rule media, entertainment, and personal communications around the planet.”

You can feel the incoherence and tension as Malone realizes that government is necessary, but also something he loathes. In the 2000s, he noticed the rise of Netflix. “Today, Netflix is the tail that wags the dog in entertainment media…. In the streaming wars, Netflix is the undisputed victor.” “No other company can match its subscriber base, infrastructure, or content investment now.”

Why did Netflix win? Of course, to Malone, it’s the big bad government and the lunatic musings of anti-monopolist Tim Wu, who coined the term “net neutrality.” That’s the regulation that prevents cable firms from price discrimination against customers. Malone argues that Netflix got a significant advantage out of the rule. “Here’s the really hard part to swallow,” he wrote. “Netflix’s business was using the wires that cable operators strung and spent hundreds of billions of dollars to upgrade, then slurping up the lion’s share of usable bandwidth - and paying almost nothing for it.” That of course isn’t true. Netflix pays a lot for its data traffic, and net neutrality isn’t in force anymore as a regulation. But truth for Malone seems adaptable.

This book came out before Paramount’s bid for Warner, on whose board Malone sits. And he had plenty to offer about the merger. Here’s his comment last November, arguing the deal is likely to do exactly what such mergers aren’t supposed to do - reduce output.

Malone believes a Netflix deal “would be much less disruptive to Hollywood. You’d have essentially more activity than less.” Whereas, if “you put it together with another studio. You’re going to try and find synergies. You’re going to have perhaps compression of activity.”

Based on what’s in this book, I have no doubt that Zazlov, who will get $1 billion in his golden parachute if the deal closes, is not making the key decisions about the sale to Paramount. It is Malone, sharp-elbowed, who is doing that. There was a bitter knock-down drag-out fight with Oracle co-founder Larry Ellison’s over how much money to throw in for the deal, and Ellison was forced to cough up a $40 billion personal guarantee with a $7 billion break-up fee. That’s textbook Malone.

There’s a lot more, including his acquisition of Formula One, his development of Liberty Media, and his sickly sweet realization that what matters is not money but the people who love you. “After years of saving, stock options, and sheer persistence,” he says. “Leslie and I have reached a point where we can finally turn outward - towards the causes we care about most: education, health, and the land we’ll leave behind.” But it’s hard to square these words with how he described his life’s work, as dedicated to building a society where capital gets a high return.

When Bernie Sanders did his “Fight Oligarchy” tour last year, the stories he told, and told by those at his rallies, were ones Democrats understand. Elon Musk pouring money into elections, rampant inequality, union-busting. Similarly, the phrase “Every Billionaire is a Policy Failure” is often understood to reflect a generic dislike of extreme concentrations of wealth, as in “they have too much, workers have too little.” After reading this book, what I have concluded is that Bernie Sanders is massively understating the problem.

Men like Malone aren’t just greedy and out for every bit of cash they can grab. They are also, more significantly, guided by a religious faith in efficiency. Money is simply the scorecard for moral achievement. This framework becomes clear when he talks about what his old mentor Magnuss would think about the shareholder returns he delivered. $1 investment in 1973 became $3950 by 2024, he notes. “Not bad, eh Bob?”

It’s a weird nostalgia, a sense of pride, for a brutal philosophy of number go up. Unfortunately, we must live in this world he shaped, and clean up the mess he made. And we must instruct an entire class of business leaders who learned their morality from a man whose vision of America is purely as a land that celebrates capital and the mobster-style leaders who amass it.

Thanks for reading! Your tips make this newsletter what it is, so please send tips on weird monopolies, stories I’ve missed, or other thoughts. And if you liked this issue of BIG, you can sign up here for more issues, a newsletter on how to restore fair commerce, innovation, and democracy. Consider becoming a paying subscriber to support this work, or if you are a paying subscriber, giving a gift subscription to a friend, colleague, or family member. If you really liked it, read my book, Goliath: The 100-Year War Between Monopoly Power and Democracy.

cheers,

Matt Stoller