BURST

BURSTDan Geller is a Staff Attorney at Antimonopoly Counsel and can be reached at dan@antimonopoly.us.

In 2023, the city of Evanston, Illinois raised its ambulance fee from $1500 to $2000, with a $15 mileage charge tacked on. Like many municipalities, city officials and taxpayers have gotten used to ever-increasing prices for basic services, all bucketed under the “cost of living” crisis we’re dealing with. In fact, yesterday the Michigan University consumer sentiment indicator hit the worst reading it has ever recorded, going all the way back to 1961. The endless increases in prices for all sorts of random necessities is a key reason.

But these cost hikes don’t just ‘happen,’ as if it’s some sort of natural event. Markets are a function of law. There are companies and dealers and financiers behind every industry, so we can actually try to understand why they are happening. In this case, Evanston chalked up the hike to, among other things, the increasing of “cost of equipment and vehicles used for emergency responses.” The ambulance market, once a decentralized set of family owned firms, has been rolled up into a consolidated industry run by private equity. And the price hikes followed.

This story isn’t unusual. In early 2025, BIG traced a roll-up of fire trucks and fire apparatus, leading to a crisis in that sector. It turns out that something similar seems to have happened here, with some of the same players.

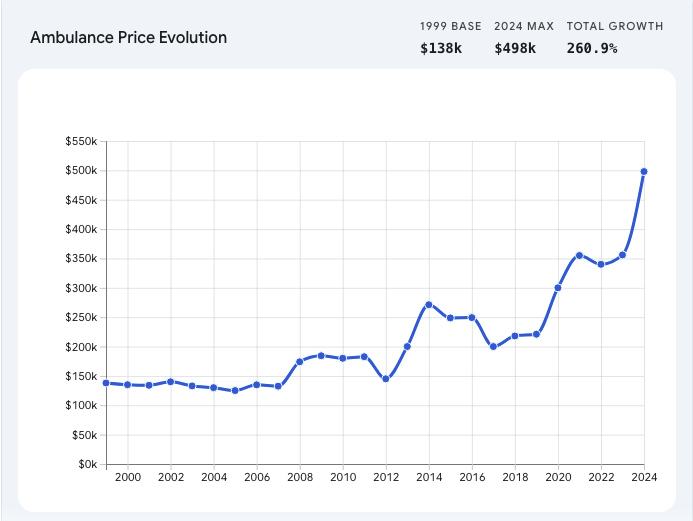

Let’s go back to Evanston. In 2011, the city purchased an ambulance for $148,000, an International MedTec used as a reserve vehicle to back up the rest of its fleet. The average ambulance is designed to last 5-7 years based on normal wear and tear. “Emergency response miles are a lot harder on a vehicle than routine traveling to work miles,” said one fire chief. But Evanston kept this one for more than 13 years, spending as much as the original purchase price on repairs to keep it going. In 2024, Evanston finally buckled down and got a new one for half a million dollars. In thirteen years, the price increased by 337% — 297% above inflation. And these vehicles are often on long backorders; in the case of Evanston, the ambulance they ordered “won’t be delivered for at least two years because of production backups.”

In 2025, North Olmsted in Ohio had a similar experience.

City Council is expected to approve the North Olmsted Fire Department’s request to purchase a new $495,000 ambulance…

The expenditure -- which is coming out of the general fund -- marks quite an increase since the fire department’s 2021 ambulance purchase price of $353,000.

“We’re seeing that across the board with not just med units but all kinds of fire equipment,” he said.

That’s not the only bad news associated with the new ambulance purchase.

“They’re telling us delivery ETA is 925 to 950 days from the date of order,” he said. “Our lead times are long now, quite a ways out. That would be 2028, so it’s gonna be a while.

“The days are gone when you could just call up a manufacturer and say you need one by the end of the year. That doesn’t happen anymore.”

We at BIG have tracked ambulance prices as best we can through public news reports, and have found that the experience of these two cities tracks the overall trend.

We have been trying to understand why these delays and price hikes are happening. We spoke with Ellen Dayan, who negotiates contracts for cities at the Suburban Purchasing Cooperative. And she told us the price for a base Horton ambulance just went up in July of last year, from $397,595 to $464,198. When I asked why, she referred me to a Horton dealer, who then referred us to a spokesperson for a private equity conglomerate, REV Group, which owns Horton and 13 other brands. That spokesperson did not respond to our questions, though the company’s most recent investor material does mention “increased … pricing of ambulances” and “higher … price realization” as significant factors behind growing revenue and profits.

“25 years of EMS and ambulance designs are stagnant,” said one commenter in an EMS channel on Reddit. “Most manufacturers are like: ‘We added a shelf for a monitor’ ‘We added a harness to the bench’ ‘We added LED cabinet lighting’ That will be $300k please!”

Emergency vehicles have always been more expensive than ordinary cars, because manufacturers must combine a truck-like chassis that can move quickly, with a platform to provide pre-hospital emergency care. Ambulances contain an HVAC system, oxygen delivery and suction services, electrical and electronic medical devices, a communications platform, and so forth. They are complex, they crash a lot, and they are packed with technology.

Like most areas of the economy, the post-pandemic era caused problems in the supply chain. Moreover, we are an aging society, so there is increasing ambulance demand in North America, where orders have grown from an estimated 6300 per year in 2017, to 8500 in 2022. Experts see the space growing by ten percent annually through 2030. The industry has blamed its inability to keep pace with rising demand on essential microchip shortages, chassis production halts leading to a 1.1 million unit shortfall in 2021, tariffs , labor shortages in the manufacturing sector, and low unemployment rates making it difficult to find reliable labor.

But there’s also been a change in the market structure. The industry was once defined by relatively stable costs—for example, Winter Springs, Florida paid $135,000 per ambulance in 2000, while Natick, Massachusetts paid $132,600 for a new ambulance in 2007, often delivered within a 120-day window.

The Roll-Up

Behind this pricing model was a competitive industry, comprised of family-owned and privately held companies serving specific regions. Major companies included Wheeled Coach (founded in Florida in 1975), American Emergency Vehicles (AEV) (founded in North Carolina in 1982), Horton Ambulance (founded in Ohio in 1968), Leader Ambulance (founded in California in 1975), Road Rescue (founded in Minnesota in 1976), Braun Ambulance (founded in Ohio in 1961), Mccoy Miller Emergency Vehicles (founded in Indiana in 1974), and Marque Ambulance (founded in Indiana in 1990).

The story of how a once vibrant industry turned brittle begins in the mid-2000s, when a private equity firm named American Industrial Partners (AIP) decided to enter the business and consolidate the makers of modular ambulances. AIP specializes in “middle market” industrial businesses; it is already being investigated by the Senate and Federal antitrust enforcers for its roll-up of fire trucks and fire apparatuses, which caused price hikes and shortages in that sector. And its work in ambulances seems to mirror its fire apparatus approach.

In 2006, AIP acquired ambulance manufacturer Wheeled Coach, an iconic Florida firm that made ambulances for cities all over the world, as well as the military, the FBI and the Secret Service. “Anywhere the president of the United States goes, there’s a Wheeled Coach ambulance following him,” said Wheeled Coach head of sales Paul Holzapfel. This acquisition marked the first step in a dramatic restructuring of the industry.

A few years after buying Wheeled Coach, AIP acquired Halcore Group, the parent company of Horton Ambulance, American Emergency Vehicles, and Leader Ambulance, which were “some of the longest standing and most respected brand names in the emergency vehicle market,” with production facilities in Ohio, North Carolina and California. That same year, AIP acquired modular ambulance producer Road Rescue from Spartan Motors, Inc. (and eventually acquired Spartan in 2020). Around 2015, AIP bundled all of the companies it acquired in the specialty-vehicle sector into a conglomerate called REV Group, which it took public in 2017. AIP retained control over REV Group until 2024, when it took advantage of REV Group’s skyrocketing stock price to sell most of its shares. Finally, last year, REV Group sold itself to another public company that makes specialty vehicles and various equipment for them, Terex.

The level of concentration is high, though we can’t get exact numbers. In 2017, REV Group told investors it controlled forty-four percent of the North American ambulance manufacturing market. Seven years later, Mike Virnig, the head of REV Group’s Specialty Vehicles division, went on the show Jay Leno’s Garage to talk to the famous comedian about the company’s new electric line of vehicles. He noted the company’s ambulance manufacturing market share is closer to seventy percent.

A different private equity firm engineered the consolidation of the remainder of the market. In 2004, Canadian private equity firm Novacap acquired the previously independent Demers Ambulance Manufacturer (Demers), one of the largest ambulance manufacturers in North America. In 2012, Westerkirk Capital Partners and Ironbridge Equity Partners acquired Demers from Novacap before selling Demers to Clearspring Capital Partners in 2016.

Clearspring then acquired Braun Ambulance and Crestline Coach in 2018, followed by Medix Specialty Vehicles in 2021. The newly-formed Demers Braun Crestline Medix (DBCM) then announced that “more than one in three ambulances in North America is built in a Demers manufacturing facility.” The numbers here are clearly estimates. Combining DBCM’s third of the market with REV Group’s estimated market share means that between three-quarters and almost all ambulances in North America are now manufactured by one of the nine brands owned by these two groups. (DBCM was sold to yet another private equity firm in 2025).

In other words, these two private equity groups seem to have eliminated independent ambulance manufacturing operations in North America.

REV Group and DBCM have faced real challenges, as every company did during the pandemic and post-pandemic era. To increase manufacturing capacity, Crestline opened a 30,000 square foot manufacturing space, Horton opened a 20,000 square foot space, and Medix opened a 7000 square foot space. But these investments have not restored the competitive dynamics of the market. And there is a likely reason for that — investors love backlogs.

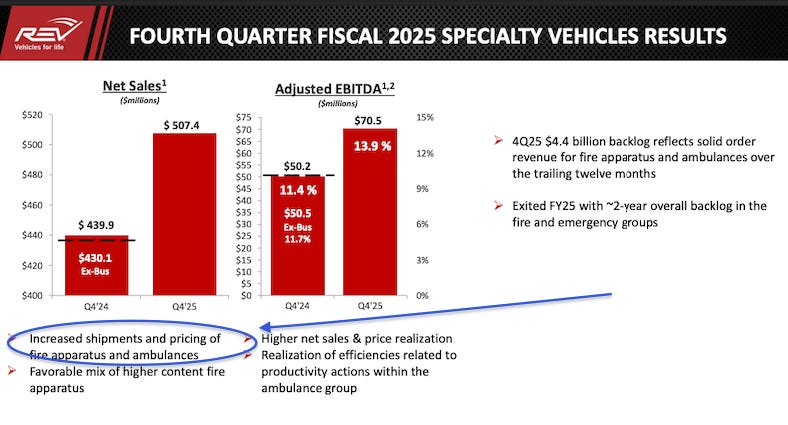

In 2025, REV Group reported almost $4.4 billion in unfulfilled fire truck and ambulance orders in their investor materials as a “highlight.” While executives have tried to blame delays on semiconductor shortages and limited chassis supply, REV Group has touted its extreme backlog as a way to increase shareholder value because it “enables strong visibility into future net sales.” And, indeed, the company’s stock price increased 640 percent in the last five years.

The consolidation of ambulance production into the hands of two conglomerates is one part of the problem, but there have also been two other changes in the structure of this market. The first is that REV Group and DBCM may be seeking to control the entire purchasing and aftermarket experience as well. Their brands rely on networks of exclusive dealers that are licensed to sell their ambulances on state-by-state or regional basis. By forcing buyers to purchase ambulances from licensed dealers while eliminating competition between them, the two dominant conglomerates appear to be enabling their dealers to further raise ambulance prices.

As Damian Rice, a paramedic in Hancock County, Kentucky noted when comparing a price increase between a 2020 ambulance purchase and a 2022 ambulance purchase, “you have to go through a dealer now,” and “[w]ith the dealer mark-up, it raised the price significantly.” Rice continued “[j]ust from when we tried to do this bid back in May, it’s [sic] went up $60,000… he said they were seeing a 20 percent increase, just on materials.”

Ford and the Chassis Shortage

The second change has to do with the platform on which ambulances are built. An ambulance is essentially the body of a vehicle, known as a chassis, with a bunch of construction on top. “It’s kind of like taking a van and turning it into an ambulance because it was cabinet work, electrical work, things of that nature,” said Scott Barnes, the founder of Wheeled Coach. The ambulance producers buy those base chassis from major automakers like Dodge, Chevy, Mercedes, and Ford. Ford alone controls seventy percent of the ambulance chassis market.1

Despite facing chassis shortages as early as 2018 (which stabilized in 2019) and Ford predicting a production shortfall of 1.1 million ambulance chassis in 2021 after a production halt, every private equity-owned ambulance manufacturer continues to rely on the major automakers for chassis. This total reliance continues despite REV Group telling its investors that chassis supply issues have lost the company up to $120 million in incremental revenue. (We contacted a number of officials at Ford and asked about chassis production, but no one responded.)

This chassis shortage and the industry’s excessive reliance on Ford isn’t a result of some inherent feature of the industry; it’s just a function of whether REV Group and DBCM want to make the required capital investment from the enormous profits they have earned over the past few years. Indeed, some of the same companies REV Group and DBCM rolled up used to build ambulance chassis. For example, in 2009, Spartan Motor Chassis (now called Spartan Emergency Response) announced the first orders, placed by then-independent Braun Ambulance, of its FurionRT ambulance chassis, which it sold through its subsidiary Road Rescue. Though the company’s time as an ambulance chassis supplier ended a year later after it sold Road Rescue to Allied Specialty Vehicles (AIP’s roll-up vehicle for this sector in the early 2010s, which it transformed into REV Group around 2015), this effort shows it is possible for these companies to manufacture chassis internally. REV’s decision not to do so despite acquiring Spartan in 2020 is indicative of a dominant market position that allows the company to spend just one percent of its revenue on capital investments in buildings and equipment, even as it faces a several billion-dollar backlog of unfulfilled orders. Indeed, one reason Terex bought Rev Group is because of its “low capital intensity,” AKA the fact it doesn’t need to invest into more production.

Since 2020, REV Group has focused Spartan primarily on supplying fire apparatus chassis to its own fire truck brands and limited fire chassis sales to outside buyers who agree not to make, or plan to make, their own chassis. Current President of REV Fire Group and REV Specialty Group Mike Virnig led this strategy in his prior role as Spartan’s Director of North American Sales before joining REV Group and pushing to acquire Spartan. In following this strategy, REV Group has boasted to investors that it has been able to “drive margin improvement actions” while reducing its manufacturing production capacity by a third.

Soon after REV Group went public, its CEO at the time, Tim Sullivan, told shareholders he expected to more than double the profit margins of the companies REV acquired from the historic norm of four or five percent to more than ten percent in short order. This followed a 2018 shareholder call where he declared “[w]e like backlog, we love backlog.” And indeed, REV Group’s choices in the face of exploding order backlogs — such as not even attempting to produce its own ambulance chassis despite owning companies that had previously done so — have proven extremely lucrative. REV Group’s Adjusted EBITDA for its Specialty Vehicles division — the best measure of REV Group’s “operating fundamentals,” according to its management’s SEC reports — has soared dramatically in recent years, increasing by $92.5 million (or 149.2%) from 2023 to 2024, and by an additional $89.7 million (or 65.5%) from 2024 to 2025.

To cope with cost increases and production delays, towns are increasingly choosing remounts, replacing only the ambulance chassis rather than purchasing an entirely new vehicle. Despite the existing chassis shortage, turnaround times for remounts are far shorter because manufacturing a new ambulance requires synchronized production of a new chassis and a new patient module (interior of an ambulance), securing a non-customized chassis to mount the module on allows for towns to bypass microchip shortages and other production issues plaguing the ambulance manufacturing market. Towns looking to save money decide to replace the chassis alone because the chassis comprises a significant percentage of the entire ambulance purchase price, and replacing the chassis by itself enables meaningful cost savings.

This trend has been brought on by necessity, as seen by Coalinga, California’s decision this past April. Rather than paying $445,000 for a new ambulance to arrive in two years, replacing the chassis alone saved $200,000, and ensured the ambulance would be in service in the next eight months. While this approach is cost and time-effective, even the chassis market seems to changed. Just five years ago, Spartanburg, South Carolina replaced its chassis for less than half what it cost Coalinga to do so in 2025.

Record wait times, backlogs, and price increases were not inevitable. Modern ambulances have been manufactured for more than a century. Up through the first decade of this century, delivery times remained stable in the 120-day range, and price increases were modest. The change in market structure removed any notion of cost or delivery certainty, leaving towns and cities across the country with no choice but to pay an ever-increasing premium for a vehicle that will most likely only be ready years in the future.

We do not have to accept this situation as our new normal. As recent congressional hearings into “America’s Fire Apparatus Crisis” made clear, we are not powerless to address markets. There are now more than a dozen antitrust cases against the fire truck oligopoly, many of which are explicitly seeking to reverse the serial acquisitions by REV Group that consolidated that industry. Overall, existing law equips lawmakers, federal agencies, cities, and state Attorneys General with tools to investigate and break-up what appears to be a PE-created duopoly in ambulance manufacturing.

We welcome any company mentioned in this article to send us a statement of reasonable length, which we will append to the piece.

Thanks for reading! Your tips make this newsletter what it is, so please send me tips on weird monopolies, stories I’ve missed, or other thoughts. And if you liked this issue of BIG, you can sign up here for more issues, a newsletter on how to restore fair commerce, innovation, and democracy. Consider becoming a paying subscriber to support this work, or if you are a paying subscriber, giving a gift subscription to a friend, colleague, or family member. If you really liked it, read my book, Goliath: The 100-Year War Between Monopoly Power and Democracy.

cheers,

Matt Stoller

In 1988, Ford launched what is now known as its Upfitter program to “offer guidelines to vehicle converters over key requirements for engineering, manufacturing, quality and process control” in converting Ford chassis for other uses. GM has a similar program called GM Envolve, while Mercedes’ is called eXpert Upfitter. Each of these companies says that Upfitter certification is not required for a downstream manufacturer to be allowed to build an ambulance using their chassis. However, all major ambulance manufacturing brands have had these Upfitter certifications for years, and they rely on them for marketing and quality assurance operations. Although from a cursory glance it does not seem like these Upfitter programs are designed to “lock” ambulance brands into continuing to use the major automakers for chassis, they may give automakers some leverage over ambulance manufacturers which is susceptible to abuse.